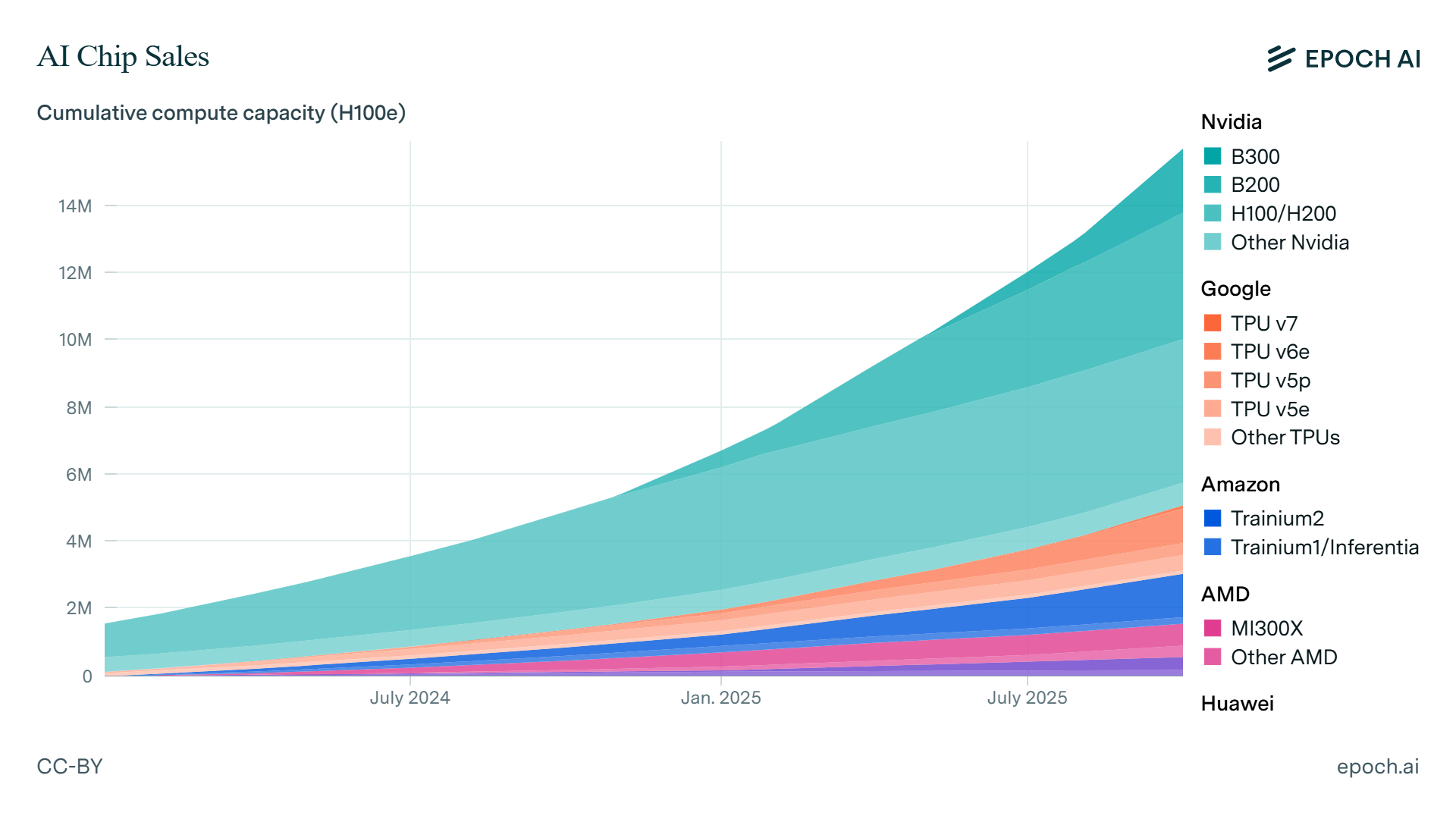

China's AI Chip Makers Seize 41% Market Share as Nvidia's Dominance Erodes

Chinese chipmakers have captured 41% of the domestic AI server market, signaling a dramatic shift in semiconductor competition as Nvidia's once-unassailable lead faces mounting pressure from homegrown alternatives.

The Chipmaker Realignment Has Begun

The semiconductor landscape is undergoing a tectonic shift. Chinese chipmakers now control 41% of the AI server market, according to recent market analysis, marking a watershed moment in the battle for AI infrastructure dominance. This surge represents far more than a regional victory—it signals the emergence of viable alternatives to Nvidia's historically unchallenged position and raises critical questions about the future of global chip supply chains.

For years, Nvidia's grip on the AI accelerator market seemed unbreakable. The company's CUDA ecosystem, architectural advantages, and first-mover benefits created a moat that competitors struggled to breach. Yet as Nvidia's lead shrinks, the narrative is changing—particularly within China's borders, where domestic alternatives are gaining traction at an accelerating pace.

What's Driving the Chinese Surge?

Several converging factors explain this market rebalancing:

Geopolitical Necessity: U.S. export restrictions on advanced semiconductors have created both urgency and opportunity for Chinese chipmakers to develop indigenous solutions. Companies like Huawei, Alibaba, and others have invested heavily in AI chip development, driven by the imperative to reduce reliance on foreign technology.

Cost Competitiveness: Chinese alternatives often undercut Nvidia's pricing, making them attractive to domestic enterprises and cloud providers operating on tighter margins. For price-sensitive segments of the market, this advantage is decisive.

Supply Chain Integration: Chinese chipmakers benefit from proximity to manufacturing ecosystems and integration with local cloud infrastructure providers, reducing friction in deployment and customization.

Performance Parity: While not universally matching Nvidia's capabilities across all workloads, newer Chinese designs have narrowed the performance gap sufficiently for many enterprise applications.

The Strain on Industry Resources

The rapid expansion of AI chip demand is creating bottlenecks across the entire ecosystem. Industry leaders report that AI demand is straining both equipment supply and talent availability, according to Tom's Hardware. This constraint affects not just Chinese manufacturers but the global semiconductor supply chain, as foundries struggle to allocate capacity and engineering talent becomes increasingly scarce.

The talent shortage is particularly acute in specialized areas like chip design, verification, and manufacturing process optimization—precisely where Chinese firms are trying to accelerate development cycles.

Market Dynamics and Implications

Recent analysis from Intellectia AI highlights the structural shifts reshaping China's AI chip landscape. The 41% market share figure, while impressive, should be contextualized: it reflects penetration within the Chinese market specifically, not global displacement of Nvidia. However, the trajectory matters more than the current snapshot.

Key implications for the industry:

- Fragmentation: The AI chip market is moving from near-monopoly toward oligopoly, with multiple viable players

- Regional Divergence: Different markets may increasingly rely on different chip architectures and ecosystems

- Software Ecosystem Risk: Chinese chipmakers must still overcome the gravitational pull of CUDA and the broader Nvidia software ecosystem

- Innovation Acceleration: Competition is driving faster iteration cycles and feature development across the board

The Nvidia Response

Nvidia remains the market leader globally and continues investing in next-generation architectures. However, the company can no longer assume unchallenged dominance in any market segment. The emergence of credible alternatives—even if regionally concentrated—forces strategic recalibration.

The real question isn't whether Chinese chipmakers will displace Nvidia entirely, but whether the industry will evolve toward a more competitive, multi-vendor landscape where customers have genuine alternatives based on performance, cost, and strategic alignment rather than technological inevitability.