Nvidia Dominates AI Chip Market Amid 2026 Competition

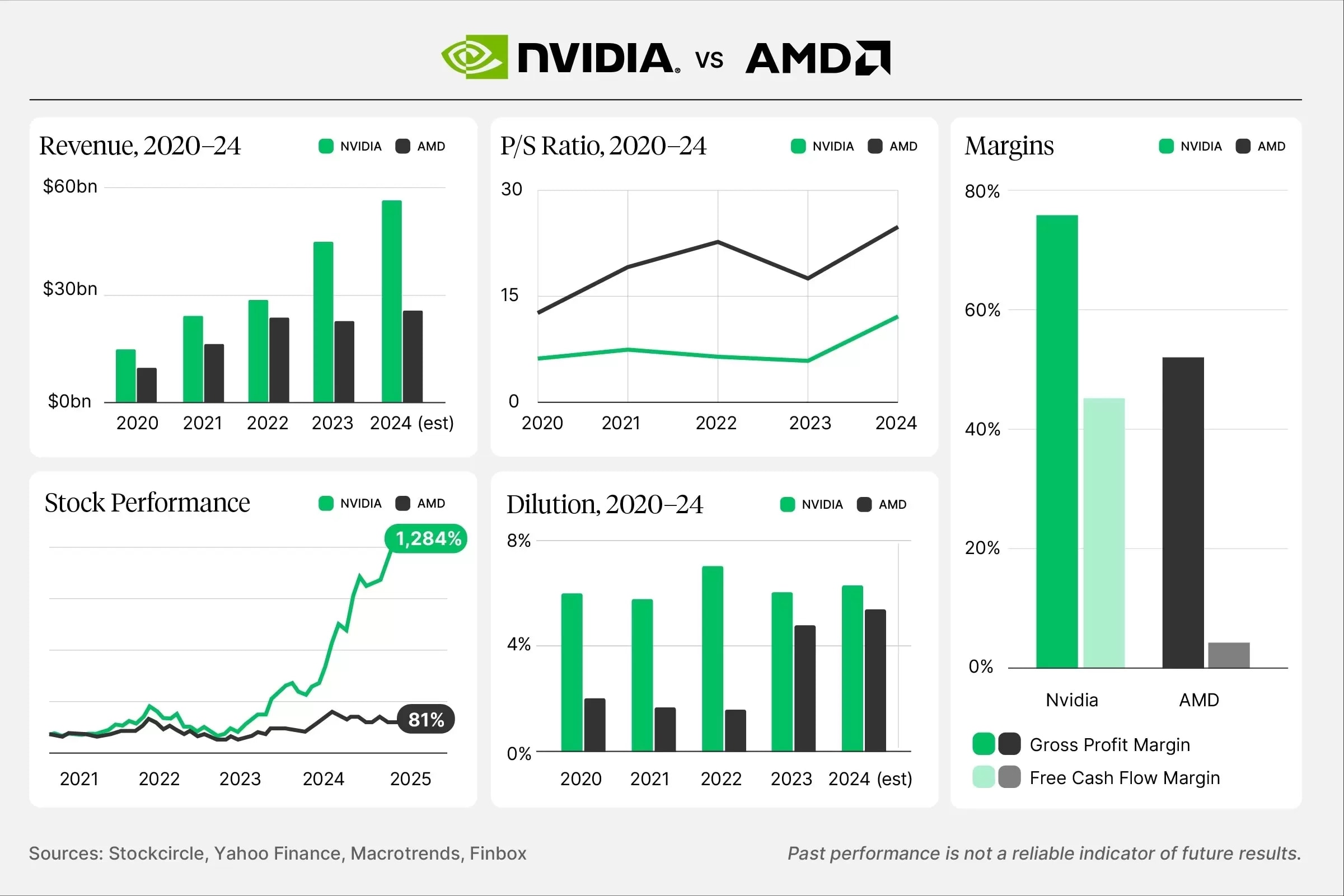

Nvidia holds a 94% share in AI chips as 2026 competition heats up. AMD struggles to gain traction amid escalating demand for AI infrastructure.

Nvidia Dominates AI Chip Market Amid 2026 Competition

Nvidia (NVDA) continues to lead the AI chip market, holding a 94% share in PC graphics add-in boards as of Q4 2025, while AMD struggles to gain ground. This dominance is crucial as the "2026 Chip War" intensifies with Nvidia's upcoming Rubin platform and the rise of hyperscaler custom chips.

Nvidia's Unassailable Lead in AI Dominance

Nvidia's market position remains strong, with a 94% share of PC graphics add-in board shipments in Q4 2025, up from 92% in Q3. This dominance extends to data centers, where Nvidia commands 80-95% market share for AI accelerators, supported by its CUDA software ecosystem.

Recent analyst commentary highlights Nvidia's momentum. Jim Cramer noted the AI infrastructure boom is "still in the early stages," with Nvidia at the center of a potential trillion-dollar buildout. Analyst Dan Ives echoed this, citing explosive growth in AI data centers despite challenges like energy shortages and geopolitical tensions.

Nvidia's roadmap is aggressive, with Blackwell Ultra ramping production, Rubin launching in 2026, followed by Rubin CPX and Rubin Ultra, and Feynman in 2028. These developments target sovereign AI, enterprise, and physical AI applications.

Financially, Nvidia's investments reflect confidence. The company announced a $2 billion stake in AI cloud provider Nebus, alongside $10 billion in Anthropic and up to $30 billion in OpenAI.

AMD's Uphill Battle: Focus on Mid-Range and Custom Silicon

AMD trails in the AI GPU wars, with its Radeon GPU strategy faltering. While AMD competes in data centers via GPUs and custom silicon, its business remains "choppier" compared to Nvidia's steady ascent.

AMD's strengths lie in cost-effective alternatives and partnerships, but it lacks Nvidia's software moat. Hyperscalers like Alphabet, Amazon, Microsoft, and Meta are developing in-house chips, potentially eroding Nvidia's share, but AMD benefits less directly.

Competitor Comparison

| Metric | Nvidia (NVDA) | AMD |

|---|---|---|

| AI Data Center Share | 80-95% | <10% (inferred from GPU shipments) |

| 2026 Roadmap | Rubin, Rubin CPX, Blackwell Ultra | No major AI flagship announced |

| Software Ecosystem | CUDA | ROCm (less adopted) |

| Recent Revenue Driver | $2.3-2.5B Q4 2025 forecast | Choppier data center growth |

| Key Risks | Hyperscaler ASICs, energy shortages | High-end market retreat |

Strategic Context Amid 2026 Chip Wars

The "2026 Chip War" timing aligns with Nvidia's Rubin launch and escalating AI infrastructure needs, including memory shortages and power bottlenecks. Hyperscalers' custom chips ramp-up threatens incumbents, but Nvidia counters with inference innovations and photonics partnerships.

Skeptical Voices and Critiques: Dan Ives warned of risks if hyperscalers accelerate in-house silicon. Geopolitical tensions and energy constraints could delay the $110 billion OpenAI raise.

Market Implications: Infrastructure bottlenecks favor Nvidia's end-to-end stack. AMD appeals to budget-conscious buyers but lacks AI scale. Nvidia offers lower risk with higher upside; AMD suits speculative plays on market share flips.

This AI chip rivalry shapes a $3-4 trillion opportunity, but Nvidia's ecosystem and roadmap make it the smarter play through 2028, barring major disruptions.