Samsung Shares Rise 5% on AI Chip Demand Surge

Samsung shares rise nearly 5% on record earnings forecast driven by AI chip demand, marking a 56% profit increase for Q1 2026.

Samsung Shares Rise 5% on AI Chip Demand Surge

Seoul, South Korea – Samsung Electronics shares climbed nearly 5% on Monday, driven by a record-breaking earnings forecast. The surge is primarily due to increased demand for AI semiconductors. Samsung projects an operating profit of 10.4 trillion Korean won ($7.5 billion) for Q1 2026, marking a 56% increase from the previous year and the highest for a January-March period. This forecast highlights Samsung's significant role in the global AI hardware market amid competition from Nvidia and others (CNBC, Reuters).

Earnings Breakdown: AI Chips Lead the Charge

Samsung's forecast underscores explosive growth in its Device Solutions division, which includes memory chips and foundry services. High-bandwidth memory (HBM) chips, essential for AI data centers, drove the surge, with sales expected to more than double year-over-year. The company reported revenue of 79 trillion won ($57 billion), up 11% from Q1 2025.

- Memory Segment: Operating profit soared to 7.8 trillion won, attributed to tight HBM supply amid AI training demands from companies like Google and Microsoft.

- Foundry Business: Losses narrowed to 300 billion won, aided by advanced nodes like 3nm and preparations for 2nm, positioning Samsung against TSMC.

- Consumer Electronics: Smartphone sales lagged, but premium Galaxy models and OLED panels provided stability.

This marks Samsung's strongest Q1 since 2018, reversing a 2025 slump when memory prices fell (Bloomberg, TechCrunch).

Past Performance: From 2025 Slump to AI Rebound

Samsung's history shows volatility tied to memory cycles. In Q1 2025, operating profit dropped 40% to 6.6 trillion won due to oversupply and weak demand post-pandemic. However, AI tailwinds emerged late 2025, with Samsung capturing 20% HBM market share by Q4.

Historically, Samsung dominated DRAM (45% share) but trailed in HBM, where SK Hynix leads at 50%. Q1 2026 sees Samsung's HBM3E chips qualifying for Nvidia's Blackwell GPUs, boosting yields to 70% (WSJ, Reuters Historical).

Competitor Comparison: Gaining Ground on SK Hynix and TSMC

Samsung now outpaces SK Hynix in Q1 profit forecasts—10.4 trillion vs. SK's estimated 8.5 trillion won. Samsung's broader portfolio gives it scale.

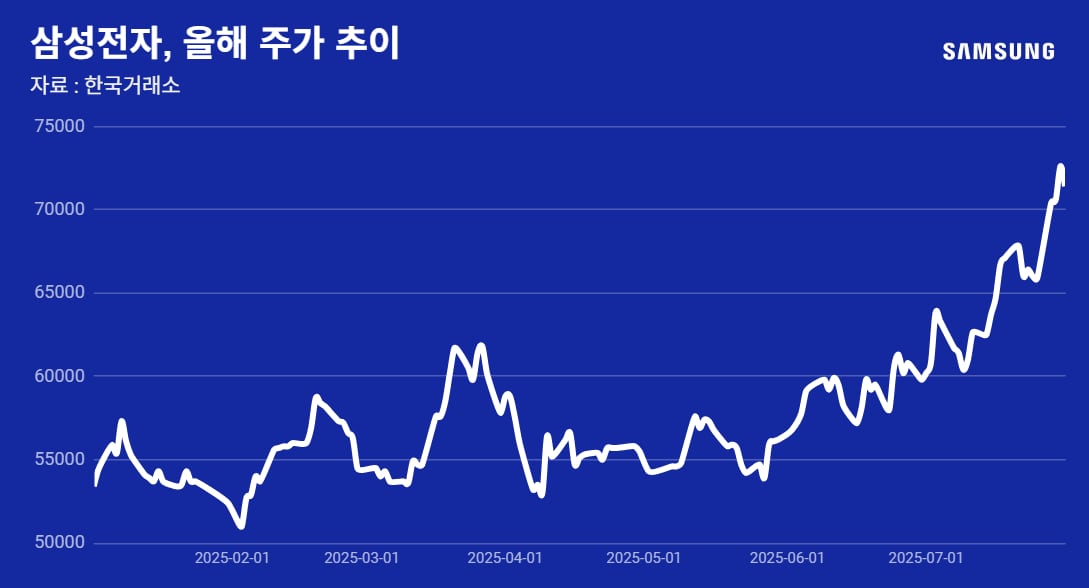

Globally, Samsung eyes TSMC, the foundry leader with $30 billion Q1 revenue. Samsung's foundry lags at 5-7% yields vs. TSMC's 90%, but AI node investments aim to close the gap. Against Nvidia, Samsung supplies HBM but competes via custom AI chips. Market reaction: Samsung's stock hit 78,000 won ($56), while SK Hynix rose 3% (Bloomberg Comparison, TechCrunch).

Why Now? Strategic Timing in AI Gold Rush

The surge ties to exploding AI infrastructure spending: hyperscalers plan $200 billion in 2026 capex, with GPUs demanding 10x more HBM. Samsung timed HBM3E mass production for Q4 2025, aligning with Nvidia's Blackwell ramp-up. Geopolitics also play a role, with U.S. CHIPS Act subsidies countering China reliance.

Strategically, Samsung pivots from consumer slowdowns to enterprise AI. CEO Kyung Kye Hyun emphasized "AI memory leadership," investing 30 trillion won in HBM4 R&D (WSJ Why Now, Reuters CHIPS).

Skeptical Voices and Market Implications

Not all is positive: Analysts warn HBM prices could peak mid-2026, potentially halving margins. Foundry challenges persist, with customer defections to TSMC.

Implications are wide-ranging: Boosts Korea's Kospi 3%, signals a memory upcycle through 2027. For investors, Samsung yields 2.1% dividends; for AI, it ensures supply diversity beyond SK Hynix. Globally, it pressures Micron and underscores Asia's AI dominance.

Samsung could reclaim its $400 billion market cap if trends continue.